Investing is the act of committing money or capital in order to gain a financial return. Investments are those things to which we commit our capital. The Investments component of the PRETIRE program plans for efficient management of your assets based on your goals, implements the plan subject to your risk tolerance, and monitors progress such that changes can be made as they are warranted.

Either you or one of your ancestors worked very hard to build the assets you possess today. Odds are that you're still working very hard to protect the assets you have and accumulate more of them. Investing is a way to make your hard-earned money make more money on its own. As you progress through your life, you'd like to see the percentage of your annual expenses that are satisfied by working shrink. This means the portion satisfied by your investments is growing, ultimately to 100%. At the point where income earned from investments can support 100% of your expenses, you've reached PRETIREment and are free to "work" or not work in whatever career / industry / opportunity you like, on your own schedule and only answering to yourself.

Please see Our Investment Philosophy, which explains how we handle Investments and Asset Management. Note that this file is a .pdf and may require you to download and install Adobe Acrobat Reader if it is not installed already.

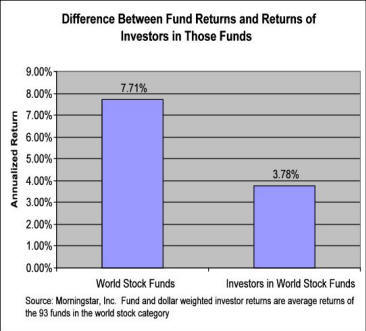

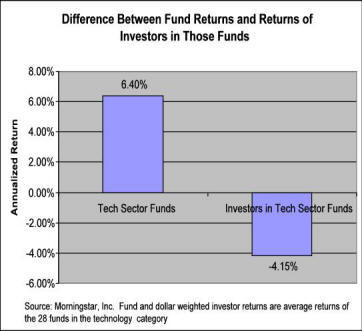

In order to manage your own investments, you not only need the time, knowledge, and inclination that you need for other components of the program, but you also need the stamina and patience to weather down markets. Investment performance is cyclical, going through bull and bear markets over time. Individual investors have been known to plow money into a market that is doing well, just in time to see it turn around. They sometimes hold on much of the way down in hopes of a comeback, only to finally give in and capitulate near the bottom, selling much of what they have in a flight to safety just before the market turns up again. As an example, take a look at the charts below.

The charts show the results of a study done by Morningstar that calculated the returns of stock funds over the a 10-year period vs. the returns received by investors in the fund during that same period. The chart on the left demonstrates the result for World Stock funds, showing that investors earned almost 4% less than the funds themselves because they (on average) bought toward the highs and sold toward the lows. The chart on the right shows the even more dramatic result for Tech Stock funds, with an almost 10% difference.

Still not convinced? A study performed by Dunbar, Inc. showed that over the 20-year period from 1987-2006, U.S. equity investors experienced an annual 4.3% return on avg vs. the 11.8% return for U.S. equities (as measured by the S&P500). The results are even more dramatic in fixed income with investors returning an annualized 1.7% vs. long-term government bonds which averaged an 8.5% return. This evidence gives further support to the theory that the average investor invests in stocks near their highs, and flees the stock market for bonds near their high, just as stocks are about to turn around.

It is human nature to lack discipline in sticking to a plan if you don't have confidence in it. And, it's impossible to have confidence in a plan if you lack the expertise to create it, and the time to implement it. Those investors who pick stocks on their own, or even those who decide to jump into the S&P500 index fund, do so feeling pretty good about their decision when the market is doing well. But, because they're not truly confident that their plan will earn the returns they need to achieve their financial goals, they can easily panic and lose discipline on a down cycle. PWA makes sure that the strategy employed to manage your portfolio is disciplined, and we're always there to remind you of that strategy when you need it.

Back to What We Offer Summary Back to Home Forward to the Next Component - Retirement Get Started Now!